Between 2021 and 2026, Canada’s patent landscape has increasingly been shaped by government-led innovation priorities rather than pure filing volume growth. Federal frameworks such as the ongoing National Intellectual Property Strategy, supported by expanded R&D and commercialization programs, have driven a shift toward strategic protection of high-value technologies and global competitiveness.

This policy focus has steered patent activity toward priority sectors including clean technologies, life sciences, advanced manufacturing, and digital infrastructure. Against this backdrop, this report presents a focused, data-backed analysis of Canada’s patent trends from 2021 to 2026, highlighting how public policy is translating into future-ready intellectual assets.

How Canada’s Consumers Are Shaping Patentable Innovation?

With 88% of filings processed via MyCIPO, the system emphasizes automation, transparency, and real-time monitoring. Internationally, collaboration with the EPO now includes AI-assisted examination and wildfire mitigation technologies.

Sovereign AI and Quantum Technology IP Capture

Budget 2025 allocates major funding to domestically owned AI infrastructure ($925.6M), quantum ecosystem development ($334.3M), SME patenting (ElevateIP expansion), and commercialization support (NRC IP Assist, Innovation Asset Collective).

A mandated IP Performance Review signals a shift from patent quantity to measurable economic impact and utilization.

SME IP Commercialization Capacity

Through ElevateIP, NRC IP Assist, and IP Ontario, Canada is strengthening startup and SME patent strategy execution.

Over 4,600 firms have received IP literacy or strategy support, with targeted subsidies covering up to 80% of eligible protection costs. The focus is on turning research into protected, market-ready assets.

Climate & Clean Technology Patent Priorities

Canada is prioritizing battery materials, critical minerals, carbon capture, hydro technologies, and wildfire mitigation.

Patent landscape analysis highlights gaps between research strength and commercial competitiveness, signaling policy intent to align innovation output with industrial deployment.

Health Technology & Biomanufacturing

Canada is advancing deployable medical imaging systems and trustworthy diagnostic frameworks such as TRUDLMIA.

Strategic investments integrate healthcare systems, life sciences, and advanced computational tools to strengthen biomanufacturing and clinical innovation capacity.

Quantum-Digital Patent Positioning

Patent clusters in hybrid quantum-classical systems, optimization platforms, and post-quantum cryptography align with Canada’s quantum priorities.

Efficiency benchmarks and scalable coordination architectures reflect Canada’s goal of practical, infrastructure-ready quantum deployment.

.

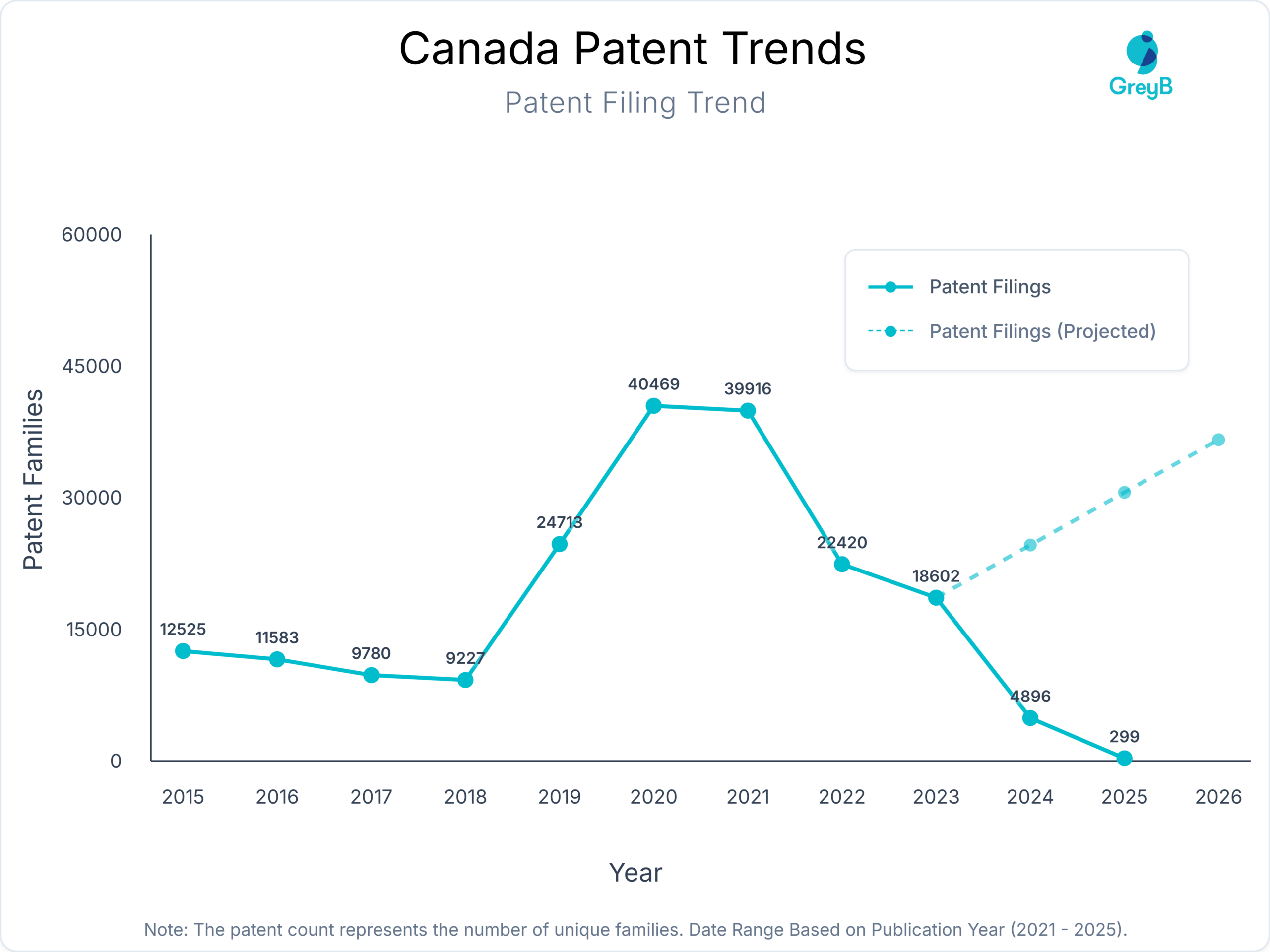

How has the Patent Filing Trend in Canada Changed Over the Years?

Canada’s patent activity follows a rise-correction-rebound pattern. Filings accelerated sharply during 2019-2021, driven by increased R&D intensity and technology commercialization.

The visible decline after 2021 is primarily shaped by the 18-month publication lag and incomplete recent-year datasets, rather than a structural slowdown in innovation. This phase reflects a data maturity effect, not weakened inventive capacity. Projected trends suggest a return to stability and gradual growth as pending applications move into publication.

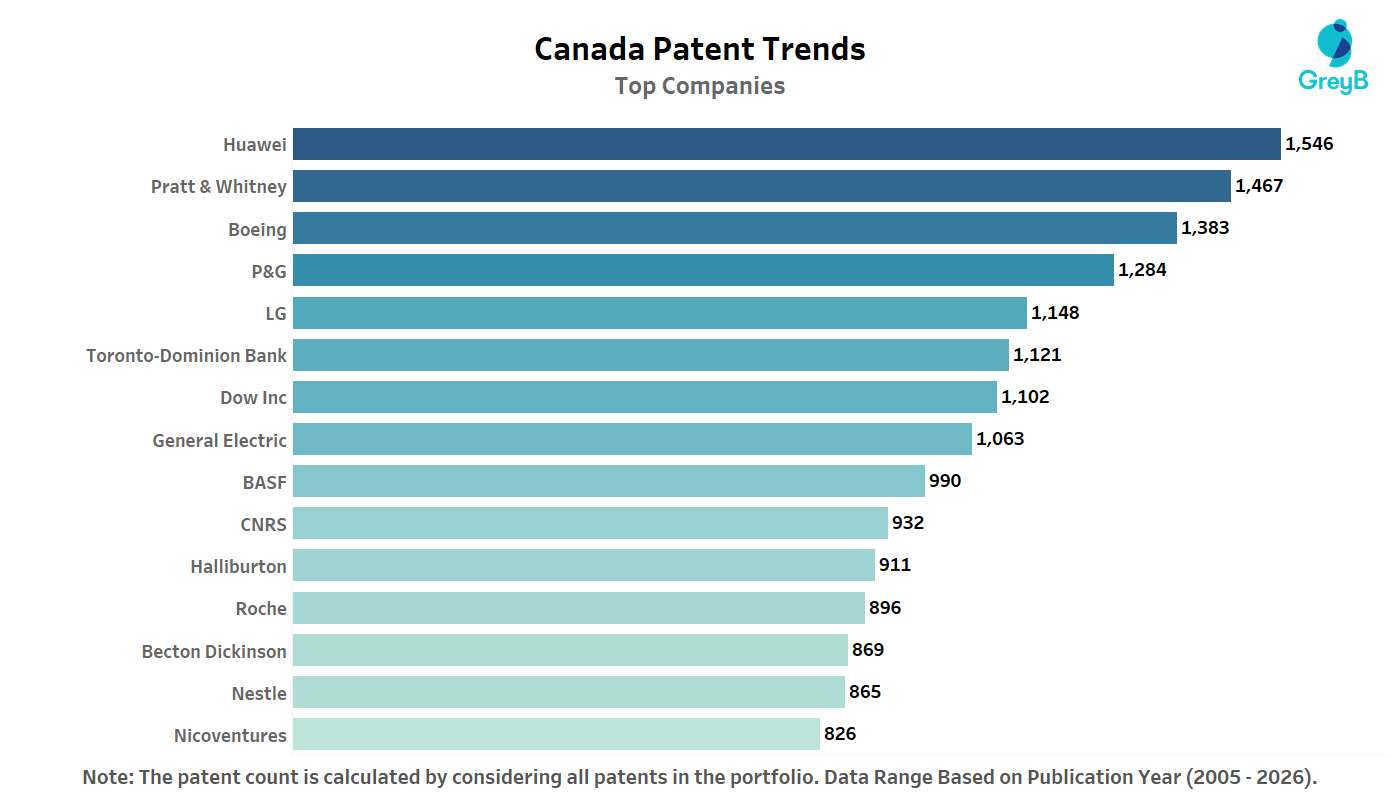

Who Are the Top Companies in Canada Patent Landscape?

Canada’s patent landscape is led primarily by multinational corporations, with technology, aerospace, chemicals, healthcare, and consumer goods players dominating filings. The presence of firms like Huawei, Boeing, P&G, LG, and GE highlights Canada’s role as a strategic filing jurisdiction rather than a purely domestic innovation base.

Financial institutions and energy majors also appear among top filers, reflecting cross-sector patenting beyond core technology domains. Overall, the data underscores Canada’s attractiveness for portfolio expansion and market protection by global innovators.

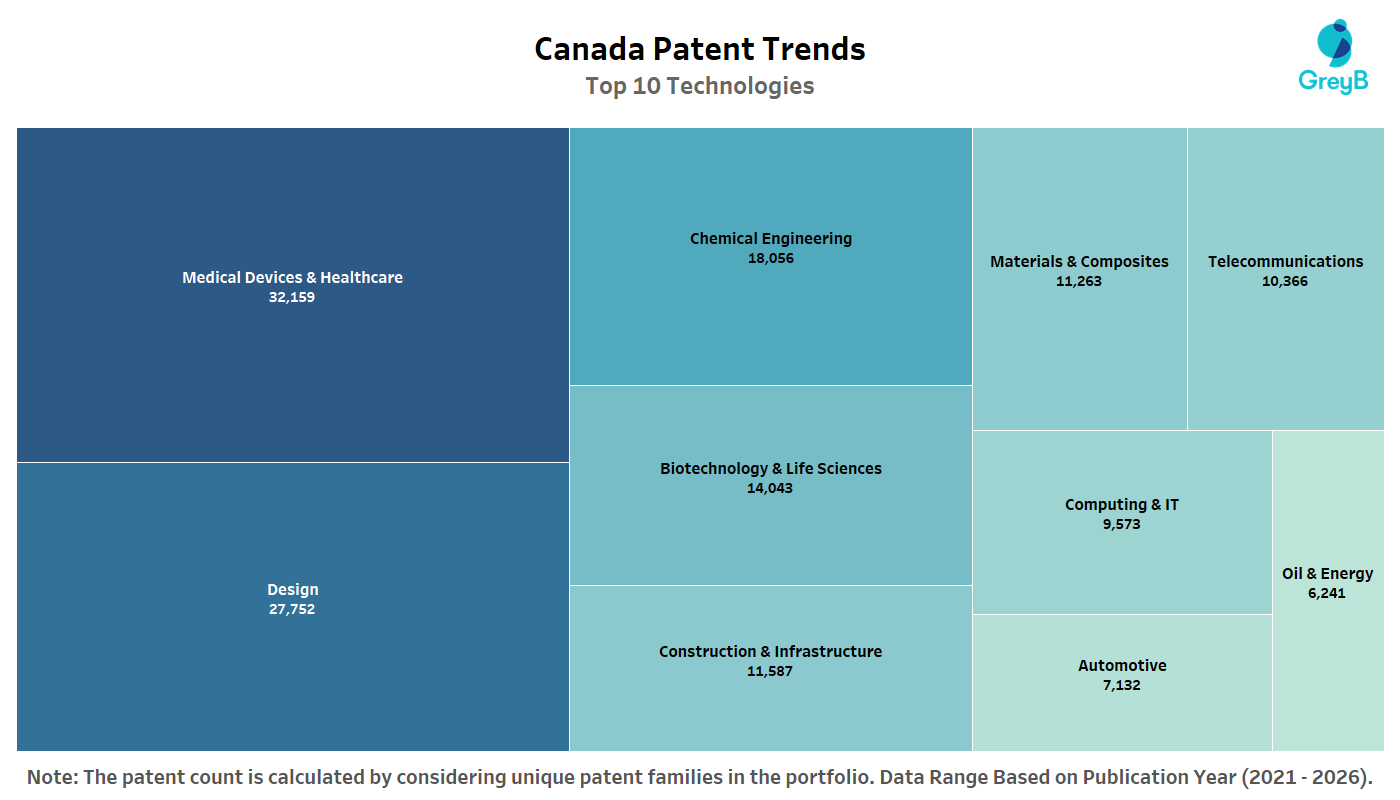

Which Key Technology Areas Dominate the Patent Landscape in Canada?

Canada’s patent activity is heavily concentrated in Medical Devices & Healthcare and Design, highlighting strong innovation around healthcare delivery, product development, and user-centric solutions. Chemical Engineering and Biotechnology form the next tier, reflecting Canada’s depth in materials, life sciences, and process innovation.

Telecommunications and Computing maintain a solid presence, indicating steady digital infrastructure development rather than explosive growth. Overall, the technology mix points to a balanced innovation ecosystem, where healthcare, industrial science, and applied engineering dominate over purely software-driven domains.

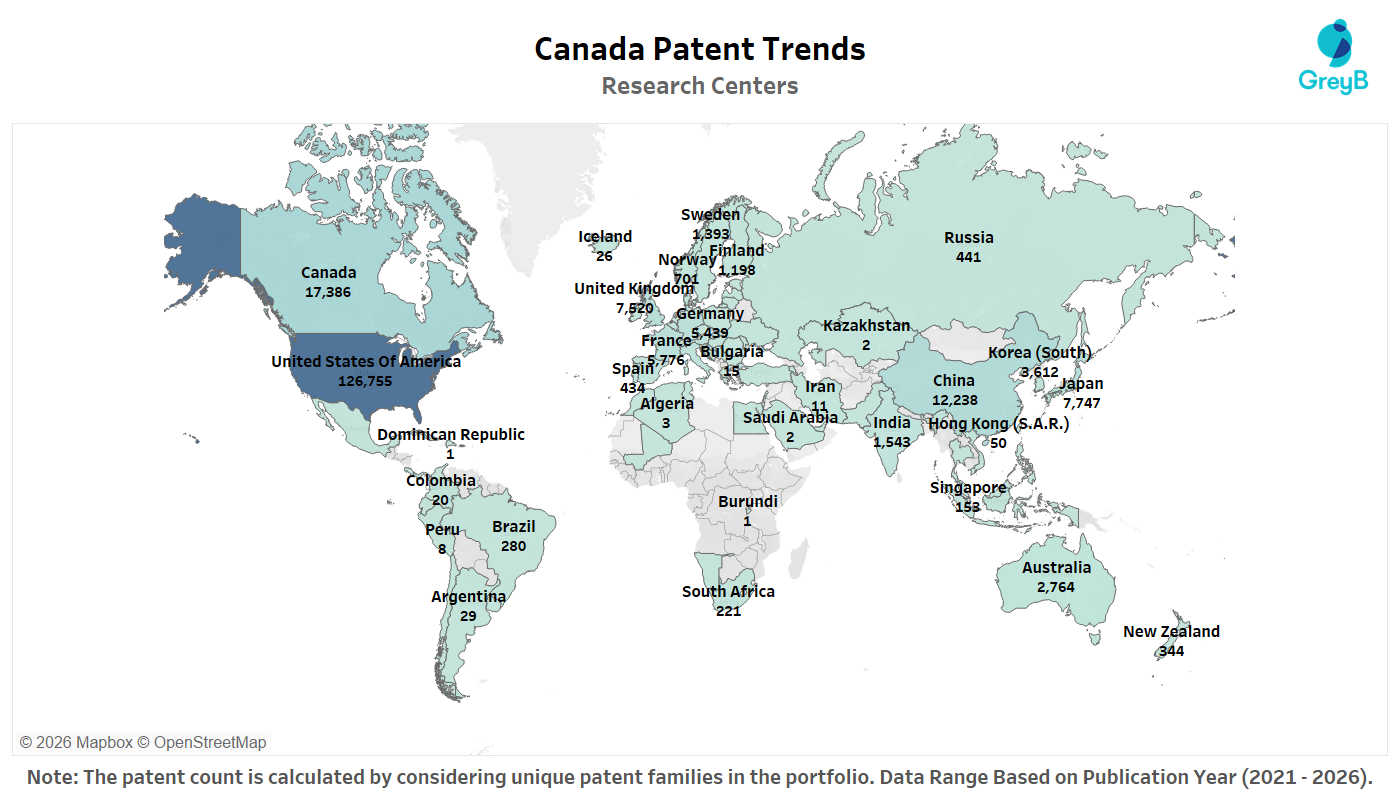

Where Are the Canada's Leading R&D Centers Located?

Canada’s patent activity is supported by a globally distributed research footprint, with the United States and Canada emerging as the primary innovation hubs. Strong research linkages across Europe and East Asia highlight Canada’s integration into global R&D networks rather than a domestically isolated system.

The presence of filings tied to regions such as China, Japan, and Korea reflects cross-border collaboration and portfolio extension strategies. Overall, the map underscores Canada’s role as a strategic endpoint for globally generated innovation, enabled by international research centers and multinational R&D operations.

Canada Innovation Prediction Roadmap

What is in the report?

Top Domestic & Foreign Companies Shaping Innovation in Canada

Evolution of Patent Filing Activity of Top Companies in Canada

Key Inventors Filing Patents in Canada

Evolution of Patent Filing Activity of Top Inventors in Canada

")